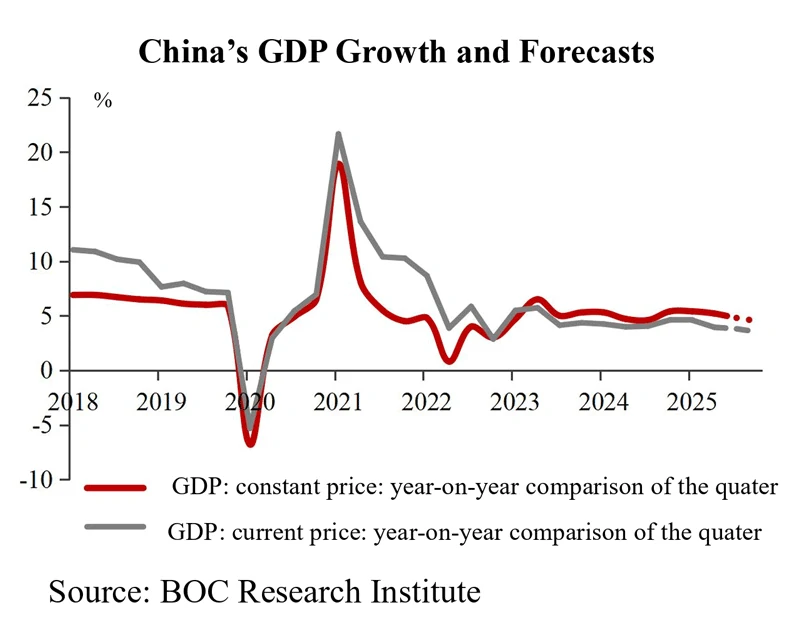

In the first half of 2025, amid the drastic changes in the external environment, China stepped up the implementation of more proactive and effective counter-cyclical adjustment policies. As a result, domestic demand was generally stable, exports performed exceeded expectation, industrial production grew fast, and the economy remained generally stable, with the GDP growth projected at around 5.4% in the first half of the year. However, due to external shocks and renewed weakening of the real estate market, economic activity moderated to some extent in 2025Q2, with GDP growth expected to be around 5.3%, down by about 0.1 percentage point from 2025Q1.

In the second half of the year, China’s economy will still face multiple uncertainties and destabilizing factors, particularly the highly uncertain US tariff policies that will weigh on export growth. It’s expected that the economic growth in the second of the year will be lower than that in the first half of the year, with GDPgrowing by around 5% in 2025Q3, and around 5% in the full year.

The necessity of intensifying and improving macro policies in the future is increasing. With the focus on the demand side, efforts should be made to accelerate the implementation of existing policies, while proactively planning incremental policies. Fiscal policies should play a bigger role in maintaining steady economic growth. Supply and demand should work in concert to unlock consumption potential and unleash the momentum of domestic demand. External risks and challenges should be guarded against, and promote cooperation and development through high-level opening-up. Stronger and more resolute steps should be taken to restore and stabilize the real estate market Industrial policies should be optimized to address prominent problems such as the mismatch between supply and demand and the cutthroat competition.